Health care quality is a huge issue in the US; despite claims that we have the best healthcare in the world, reality is far different.

Why? I’d argue its because healthcare consumer behavior drives our for-profit system.

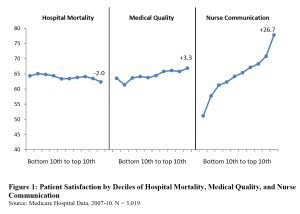

What makes patients happy is completely unrelated to the actual quality of medical care they receive – or how likely they are to die.

Research article is here.

the horizontal axis indicates hospital performance by deciles for each category…note patient satisfaction doesn’t vary by hospital mortality and varies just a little by medical quality, but varies a LOT by nurse communication.

The effect of nurse communication on patient satisfaction is four times larger than the effect of the hospital’s mortality rate. Yup, as long as the nurse smiles, is responsive and nice, we’re satisfied. Never mind if we’re a lot more likely to die.

Another oft-measured factor, the quietness of the rooms, has a 40% larger effect on patient satisfaction than medical quality.

This is because hospitals provide two separate and distinct kinds of services – the technical delivery of medical care and “room and board-related” services. Patients are much better at observing and rating the “hospitality” part of their hospital stay than the medical care they get.

To quote the authors;

Hospitality is the fast track to customer satisfaction in medicine.

What does this mean for you?

Customer satisfaction is the fast track to profits… not to good medical care.