OK folks, deep breath here. Let’s take a minute and discuss what’s really going on with the ACA.

ACA – or the more-commonly-used-but-nonetheless-inaccurate-title Obamacare ≠ the Exchanges. I don’t know why pundits, pols, and regular people don’t understand this.

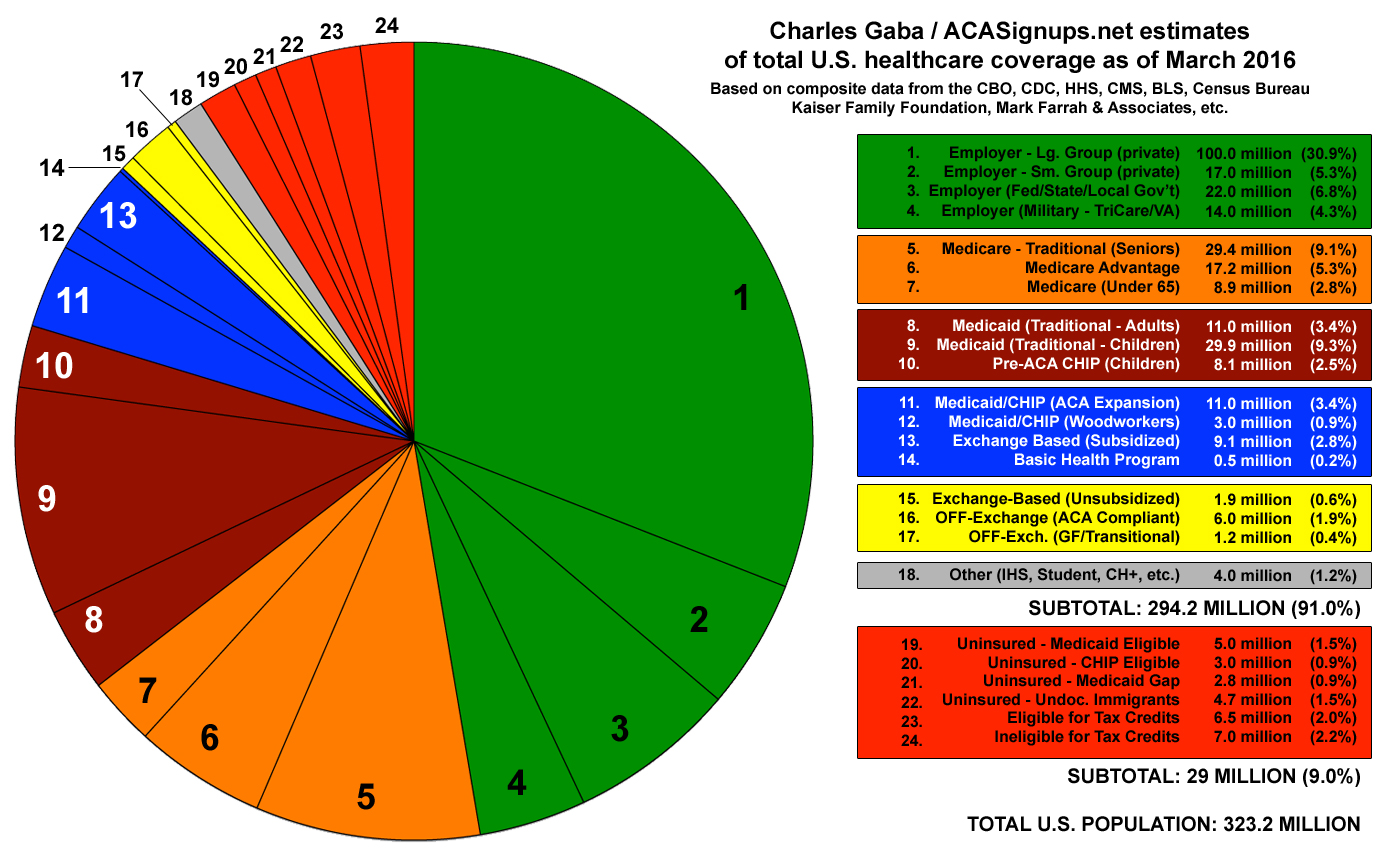

Let’s remember that enrollment in the exchanges and individual plans amounts to about 6% of all insureds in the United States.

Six percent.

Second, remember that the ACA includes a lot more than just the exchanges.

Elimination of pre-existing condition clause, guaranteed issue, coverage of dependents to age 26, Medicaid expansion, changes in Medicare reimbursement all have much more impact on the overall industry and population than the exchanges.

It’s clear that rates in the exchanges are going up a lot. This is because there are not enough young people and healthy people buying coverage on the individual market to offset the expense of us older folks. And, it’s because the big commercial plans aren’t very good at individual coverage.

As the penalties for failure to obtain coverage increase, we can expect more people to enroll in health insurance. But for now, rates are going up significantly.

That said, I can say from personal experience that our rates are going up less than one dollar for a platinum plan in upstate New York. We are enrolled in a very narrow network with no out of network coverage.

The big commercial plans, United healthcare, Aetna, Wellpoint are all experiencing significant losses in the exchanges. However the plans that are more locally focused and have more expertise in Medicaid and other individual markets are doing well.

Therein lies a lesson. The big commercial plans are very skilled and very experienced in dealing with employer plans. However their expertise is not in the individual market which is why they are getting crushed.

Let’s not forget the ACA is based on private insurers competing. The competitive market is working. As the plans that can’t compete are exiting Exchange markets others are earning more business. This will, over the long term, help control cost and deliver better care to individuals on the exchanges. And, it will make these individual market winners better able to compete for employer business as their cost of care is going to be lower.

Finally, unlike most major federal legislation, there has been no effort on the part of the opposing party to fix the problems with the original legislation.

Hopefully this will be remedied under a new administration.

What does this mean for you?

Progress is painful. But reforming our health care system is absolutely necessary.

Joe, I think the point you are missing is that the big healthcare carriers are increasing ALL premiums to make up for those ACA losses. So everyone is losing!

Hi Bob – thanks for the comment. I haven’t been able to find a source that speaks to your statement; can you share ?

thanks Joe

Arizona, where I live will be hit the hardest with astronomical rate increases. An individuals projected rate increase will be in excess of $400 per month, while a family of four premiums is will stretch to $1450 per month.

Obama care is a big lie and it was sold to the American people as a big lie. Drastic changes need to be made in an effort to make it “Affordable” The two biggest lies about Obama care are “I could keep my physicians and my premiums would drop”. One of very few things I agree with about ACA is that insurance companies have to cover pre-existing conditions.

I’m not sure scrapping it is the answer, but a significant overhaul needs to be made.

I agree. My individual plan for the wife and kids has jumped almost $400 extra a month. It is crushing a lot of middle class people. It is socialism at its best and I am in shock that the American people would vote for the candidate that supports the continuation of Obama Care. Sorry I can’t call it the Affordable Care Act because it is far from affordable. This is my personal experience.

Hi Spencer – the issue is the underlying cost of health care. As I noted, my narrow network/no out of network plan went up $1.00 for 2017. I assume your health plan is a for-profit or nominally not-for-profit; regardless, the onus is on them to develop a plan, coverage, and a network that delivers what you want. If it is too expensive, switch.

You mention that if a plan is too expensive, switch. Hard to switch to another plan when there is only one carrier offering insurance via the exchange in my state.

I agree, the healthcare needs to be reformed. Lets start with Big Pharma and let the government negotiate pricing. It is all a crock.

This is my reality and there are no pie charts that capture that; as a consumer ACA is crippling my ability to build wealth, save money, and invest in my future. The out of pocket, deductibles, and coinsurance are eating us alive. My only hope is to hang on and get my spouse and myself into MediCare and a supplement plan. The government should never have been allowed to get into the insurance business. If they were concerned about access to healthcare well then build the clinics and hospitals, hire the staff and deliver healthcare.

The large plans are getting crushed because the ACA is the king of “adverse selection”: You must accept pre-existing conditions, lots of mandated benefits, can drop your plan after receiving services, low penalties for not carrying coverage. Health insurance only works when the well pay for the unwell. ACA has attracted lots of unwell people and fewer well people. I’m only surprised that it’s taken this long for the costs to pile up.

Gene

Thanks for the comment. No question many of those issues need to be addressed in clean-up legislation.

::steps on soapbox:: When I was Benefits Manager for the State of Arizona 10 years ago, we moved the employee health plan to a self-insured model because of fully-insured premium increases of 15-20% annually. At the time, the Trust Fund was $550 million, so you can imagine what those increases were doing to an organization that big. As a large employer, some of those premium costs were absorbed by the State in lieu of pay increases. Unfortunately, in doing so, premiums were kept artificially low for the employee- $25/mo for single coverage and $150/mo for family. The perception of what health insurance really cost was altered- I\’m sure this was done with a lot of employers. This altered perception most likely plays into the \’sticker shock\’ most now see in their employer-sponsored plans as employers shift more of the burden to employees and eliminate expensive HMO\’s and POS plans for high-deductible and HSA\’s. In Micheal\’s statement above, $1,450/mo isn\’t that alarming for a family of 4 (the person would probably pay less due to subsidies applied) given the uninsured population is typically unhealthy since chronic conditions aren\’t maintained, unable to afford screenings, etc.

Rising healthcare costs are nothing new- it was a problem we faced long before Obamacare. Hospitals have always increased rates due to uninsured patients showing up in emergency rooms and Medicaid (AHCCCS in Arizona) programs swelled due to indigent people needing medical care- Americans have been paying the cost in rising federal/state/county taxes or hospital bills whether they recognized it or not.

The critical issue- until such time as a NATIONAL emphasis is made for people to take personal responsibility for their own (and family) health- i.e. diet, exercise, appropriate screenings, quit smoking, etc., Obamacare or whatever they replace it with are all Band-Aids over a gaping wound. And it\’s only going to get worse with rising obesity rates and chronic conditions in children and adolescents. Until we sufficiently address this issue, any adjustment or replacement for Obamacare will be like fixing a dam leak with bubblegum.

::steps off soapbox::

Well said Susan.

Having health insurance is critical and we need as a country to find a way to provide it to everyone. Imagine your 3 year old falls off the monkey bars and breaks her arm. You take her to Urgent Care and they say she needs to go to the hospital to see an orthopedic surgeon. You take her to the hospital. They admit her and you say overnight and go to surgery the next day. You are discharged at 10pm after surgery. If you have insurance you will have some out of pocket costs, but if you don’t have insurance you will have a WOPPING Bill on your hands.

Our country can afford to ensure every person is covered. We just have to stop complaining and bite the bullet.

If I remember before the ACA individuals could buy individual plans from all the large carriers. Including PPO, HMO and POS. With good networks. Now those same large carriers (UHC, Aetna, Wellpoint and a lot of Blues plans) no longer offer individual plans because it has to be funneled through the exchanges. What happened with just going direct? Unintended consequence I guess.

Also, are dependents really covered to age 65? :-)

Jeff – great catch – blush – maybe dependents are those OVER 65!

Health plans can offer individual coverage thru their own distribution channels; they don’t have to use the state/federal Exchanges unless they choose to do so. they

Thanks Joe.

Can you share with us all those distribution channels examples? Insurance broker? Direct with the carrier? Financial advisor?

Reason I ask is we can all learn from it and I cant seem to find any of those channels. UHC – only offers direct for short term Golden Rule Plan. My insurance agent says plans are only offered through the exchange. etc. Anthem – only gives me options that are on the State Exchange.

Hey Jeff – agents and brokers are one channel; private exchanges – https://obamacare.net/enroll-now/ and https://www.healthinsurance.org/quotes/ are two examples. You can also buy direct from a health plan.

Joe,

I share your frustration of the continual use of ObamaCare to refer to the individual health insurance market. What will they call it in two weeks? Also agree that all new major policies need incremental change and adjustments–something that has been impossible with constant calls for repeal and a deep-seated desire by the ACA\’s opponents to see it fail. If it does, how does that help the tens of millions who gained coverage under the law? What we had before was truly unsustainable.

Folks are deflecting the real culprit, which is not the ACA, but our system in general; a system where few have real skin in the game and everyone feels entitled, and where there is no meaningful competition, we overpay for drugs and devices (we can’t legally buy overseas where the same drugs are a fraction of the cost here in many cases), lack of transparency in costs, and no downside for most to consume. The good news is that the double digit increases my company has seen in many recent years for insurance has reduced to a more moderate increase well above inflation. Before the ACA, many went uninsured and when something happened, they would not, could not pay, and the tab is picked up by the rest of us. The claimed adverse selection we hear of now, was a big reality then, and folks with preexisting issues were priced out. One of my kids works for a small startup and has to buy his own coverage. It is high deductible but is there if he needs it. Absent the ACA, not sure how available and at what cost.

Those who choose to trash it and Obama’s role should answer this: Was it better before, and if so, for who? And if it went away as Trump promises, what exactly should follow it? Also, I assume for consistency that since government in the health business is evil, that you will sign off in the end of Medicare, Medicaid and the Veteran’s Health Administration – and have a good idea as to what will replace all three?

Joe, put the Kool Aid cup down! It has a big hole in the bottom of it! (: We need your help on the WC issues and your distraction on defending this hurts us all in this industry!

John – WC issues and ACA are inextricably linked. In fact, a major problem in the work comp industry is a failure to understand that work comp is 1.25% of total US medical spend. Put another way – things happen TO work comp, work comp does NOT control anything.

If one does not understand major drivers in the health care system/industry/ecosystem, one will be surprised and ill-prepared to deal with the repercussions. For example, MACRA affects fee schedules – how have you prepared for this? The non-expansion of Medicaid has increased hospital costs in those states – how does this affect your clients and their loss ratios?

Moreover, industry-derived analyses of the impact of ACA often are authored by staff that either have ideological biases or just don’t understand the bigger picture and therefore draw wrong conclusions or make inaccurate statements. There are a number of misunderstandings of ACA and the potential impact thereof in documents such as this one.

Finally, I don’t think what I write “hurts” the industry, it just upsets people who don’t want to consider different opinions. Rather than complain about what I write, you may want to consider it objectively. That will help you help the industry.

Joe,

I believe you are mistaken when you say the “opposing party” which I guess are Republicans, have made no effort to fix problems with the original legislation.

In addition to the many changes made by the administration via mandate, there have been many laws enacted by the Republican Congress, with bi-partisan support and signed by the President, to address short-comings in the ACA. I believe many were enacted within the past 12 months.

I recall an article in either Money or Forbes fromm earlier in the year (which I can’t seem to find right now) that discussed the number of changes to the original law. I think the article referenced a study by the Galen Institute (?) that analyzed those changes.

Mike – thanks for the note – always good to hear from you.

Galen did publish a list of changes, however many are far from improvements, but rather intended to inflict “death by a thousand cuts”. Most were passed as part of budget bills, and were NOT supported by Democrats or the President e.g. cut to IPAB, eliminating risk corridor payments, defunding co-ops, etc. They were signed into law as the refusal to do so would have closed down the government. Much of the rest were very minor changes e.g.adoption credit, TriCare extension, etc.

http://galen.org/2016/changes-to-obamacare-so-far/