The US healthcare system is costing you $8000 more than it should. That’s because you – the consumer – are at the mercy of hospitals, insurers, doctors, device companies, pharma.

You know this.

You know the healthcare “system” is designed to make money for healthcare providers, big pharma, device companies, healthplans – not to help you and your family stay healthy and functional.

You know the healthcare system makes money – buckets of it.

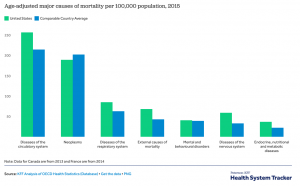

You know we spend way more than any other country, yet we die younger.

You know Purdue Pharma made tens of billions of dollars addicting your neighbors and kids, and got away with it for decades.

You know this because the hospital industry has never been more profitable. Oh, and rural communities are losing hospitals because those hospitals aren’t “profitable” – despite the fact that rural Americans are losing access to desperately needed healthcare.

You know this because you can’t “negotiate” with your local hospital, or insurance company, or pharmacy – because they have all the power and data and political influence, and you have none.

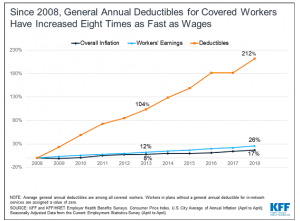

You know this because your healthcare premiums and deductibles and out of pocket costs keep climbing – and your wages don’t.

Healthcare is not, and cannot ever be, a free market. A free market requires buyers have the ability to make sellers respond to buyers’ needs – yet we all know we consumers have zero ability to make pharma, hospitals, big doctor groups, device companies respond to our needs.

How dysfunctional is this “healthcare system” that costs you $8000 more than it should?

Well, imagine if air travel was like healthcare…(link opens video)

This is why your family is paying the healthcare industry $8000 more than you should – the industry has all the power, we have none.

What does this mean for you?

This will continue until you decide it won’t

LOVE the video…but I am sorry to say, the airline reservationists gave MUCH more info than a healthcare insurance customer service person knows……in reality, healthcare is not far away from this……….everyone needs to know how to be their best advocate. I am writing a series of blog posts to help people become their best advocate and know how to ‘function’ in a dysfunctional system. Here is the link https://nursesadvocates.com/focusing-in-on-the-new-kid-in-town

Anne – thanks for the comment – and for sharing your advice!

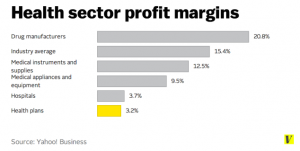

Hi Joe, thanks for the article. I have a question and you may or may not have the data, but how much of the drug manufacturers revenue and/or profit is driven from over the counter vs prescription medications? Thanks

Thanks for the question Marko.

OTC revenues are about $180 billion; Prescription Rx twice that.

https://www.statista.com/statistics/307237/otc-sales-in-theus/

https://www.statista.com/statistics/184914/prescription-drug-expenditures-in-the-us-since-1960/

Joe, The frustration is palpable. You mention insurance carriers/health plans. Some may understand why, as middlemen, insurers are in a position to control pricing and/or benefits and thereby become the “front” for big pharma, health care providers of all types, etc. Not to defend the billed charges submitted by many front-line providers, but where would one find data that show the nature and extent of insurer deals with the providers – deals that end up funding their huge profits? Another way to ask the question might be, is there data that show insurers are complicit with the providers you mention in making care more expensive than necessary?

Hello Steve – thanks as always for the comment.

There is little evidence to support your contention that insurers are in any position to control health care prices. In fact, as I’ve reported here extensively, the opposite is the case. Healthcare providers have increasing pricing power due to massive consolidation.

Second, what “massive profits” are you referring to? Again, all the evidence indicates health care providers pharma and device companies generate much higher returns than insurers.

Please provide any data you have to support those assertions.

These margins and data are pretty wild. Thanks for sharing Joe.

My insurance premiums hit $21,564 in 2019 and basically all I got out of it was a free lipid panel test valued at about $102.85. If my wages increases were tethered to the trends we are seeing in deductibles and insurance premiums or if I had some of these premium dollars in my pocket/invested over the years, I probably could have retired at 35 instead of 40.

Max

Medical prices have increased for 52 years since 1966. The health benefits consulting, brokerage and insurance industry has operated using the same inflationary silo model that prevents the positive interrelationships between claims, information, prevention, productivity, processes and profitability from being realized. Once silo risk is eliminated and demand-based interventions flow through a deflationary integrated model health cost inflation can be eliminated. As the dearly departed Jim Palmer, former Health Risk Integration Manager for Procter & Gamble’s successful effort that eliminated health cost inflation for a decade from 1990-99 said, “Demand side success will force supply-side capitulation.” He also said some other things that I’ll save for another post.

Hello Frank – The problem with US healthcare costs is price.

If buyers start forcing better pricing, results will follow. Not sure how integrating all those services solves that problem; work comp medical dollars represent <1% of total US medical spend so there's not much spend to leverage.