Over the last decade I’ve worked with over 30 investment firms on perhaps 60 deals. One question I almost always get is:

Would you buy this company?

And a related question:

What would you pay for this company?

For years I tried to answer those questions, factoring in the company’s service reputation; the uniqueness of it’s services and/or business model; experience of management; value delivered to it’s customers; and a bunch of other stuff.

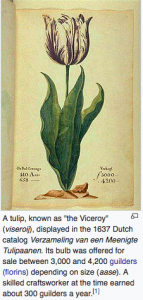

I finally realized those criteria often had little to do with the “value” defined by most investment firms. And much more to do with Dutch Tulips.

To most private equity firms, “value” is what can they sell the company for in a few years. One would think the selling price would be driven in large part by those other criteria; in many cases, one would be wrong.

Recent valuations of some work comp service companies are – in my view – completely disconnected from the actual value inherent in these companies – actual value defined as the value they bring to their customers and the potential for those companies to grow and prosper.

In fact, what seems more important than actual value is the ability of the seller to craft a story about how the company is going to grow, it’s unique business model, it’s scalability and potential to be a platform to which other acquisitions can be added. This is typically future-forecasting, theoretical stuff based on assumptions thin enough to blow away in the slightest of headwinds.

But more often than not, enough potential investors buy into the story to create a bit of a feeding frenzy, until one agrees to pay way more than that company’s actual value.

I’m far from an investment expert – one look at my personal portfolio will prove that – and in no way am I saying the brilliant folks at private equity firms don’t know what they are doing. Far from it – these people are doing exactly what they are supposed to do – make gobs of money for their investors.

What I am saying is these firms are rewarded when they sell the companies they bought for a lot more than they paid. That works out really well – if they can find someone to buy it at a hefty markup. At some point the next owner – or the one after that – finds out that the actual value of that company is far less than they thought.

It’s also known as the Greater Fool Theory, or the Dutch Tulip problem. You know the asset isn’t worth what you’re paying, but you’re sure you can find someone else who will pay more than you did.

What does this mean for you?

Beware of tulips. They flourish until winter comes. And winter ALWAYS comes.

Great article Joe. Thoughtful comparison to the first cartel and resulting price shocks. I really like it when you focus on insurance issues rather than politics.

Tom – thanks for the note and glad you liked the post.

We agree – I much prefer to talk healthcare than politics. Unfortunately, the two are inextricably intertwined, and therefore it is inescapable.

Joe, a very good overview on private equity (PE). Taking off from your high level view, the generalization on how PE’s attribute value is fine tuned by what the fund’s appetite and investment thesis and time horizon for their exit are. For folks in workers comp looking at contracting with PE owned vendors, something to consider is how far into their investment the service provider’s PE owners are. If they are getting close to say their typical five or seven year holding period, then you should factor in the potential disruption from a sale of that vendor.

Marc – thanks for the comment – excellent point.

I’d add a tiny clarification for those not deep into this world; PE firms typically have several investment funds, so make sure to identify the one that has invested in the service provider you are focused on.