Frank Pennachio is one of those people every industry really needs. He’s blunt, outspoken, deeply insightful and completely unafraid to challenge established practices.

Especially when those practices need to be challenged. Thursday at NWCDC, Frank and Denise Algire discussed the ways employers pay for managed care services, and how those are often disconnected entirely from the quality of the care delivered to patients.

Frank’s key question is this; do managed care programs improve care or create revenue for intermediaries?

My take is both. I’d also echo Frank’s view that employers and brokers are just as culpable, if not more so, than claims payers and managed care companies. Employers’ desire for simplistic fee arrangements and unwillingness or inability to dive deeper into fee arrangements force (or allow, depending on your perspective) TPAs to seek revenues elsewhere.

Transparency is what’s missing; contracts between and among TPAs and employers don’t allow employers to see the financial relationships between the TPA and managed care companies and providers and understand the motivations and incentives inherent in those relationships.

Fee arrangements are the key to the puzzle. TPAs charge employers a flat per claim fee or a loss conversion factor (losses x X.XX%) to cover the cost of handling claims, and that’s pretty much the only thing the employer looks at or cares about. Thus, allocated loss adjustment expenses are rarely addressed. What employers should be paying attention to are undisclosed side agreements and Allocated Loss Adjustment Expense bucket, where those fees end up charged to the file.

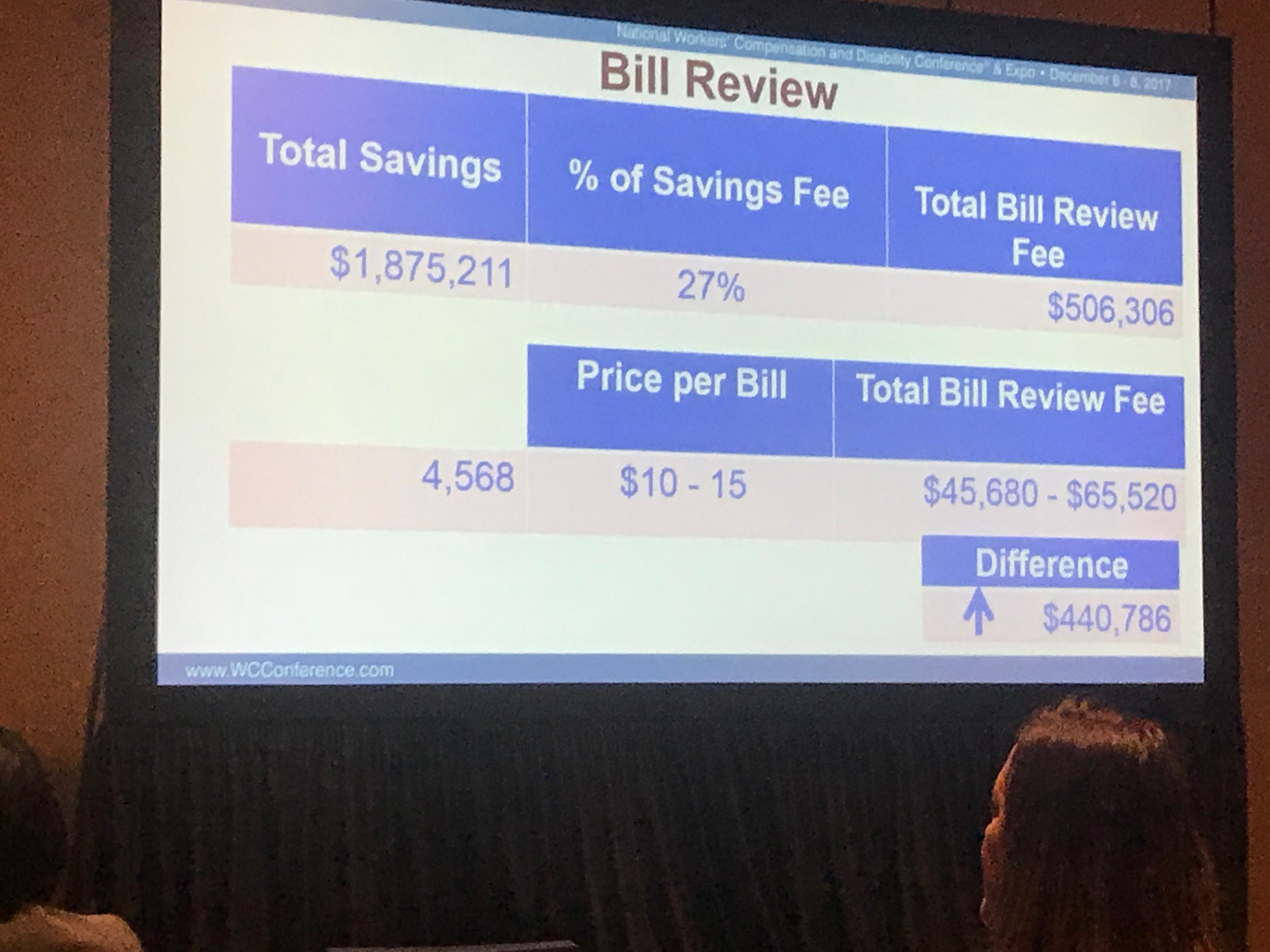

Frank showed a report from an employer that identified bill review fees of over $500,000 for some 4600 bills. Of course, this was based on a fee structure using a percentage of savings below billed charges – an arrangement that like vampires just won’t die. Frank noted that many bill review companies are quite willing to charge a flat per-bill fee that includes networks, medical management, and other “savings”. (I have a somewhat different perspective and believe the price per bill should be considerably higher, but fundamentally agree with Frank) Part of me is stunned that we are still talking about this. This has been a subject of conversation many times over many years, and yet, here we are. And here we’ll stay until and unless employers demand something different – and

Part of me is stunned that we are still talking about this. This has been a subject of conversation many times over many years, and yet, here we are. And here we’ll stay until and unless employers demand something different – and

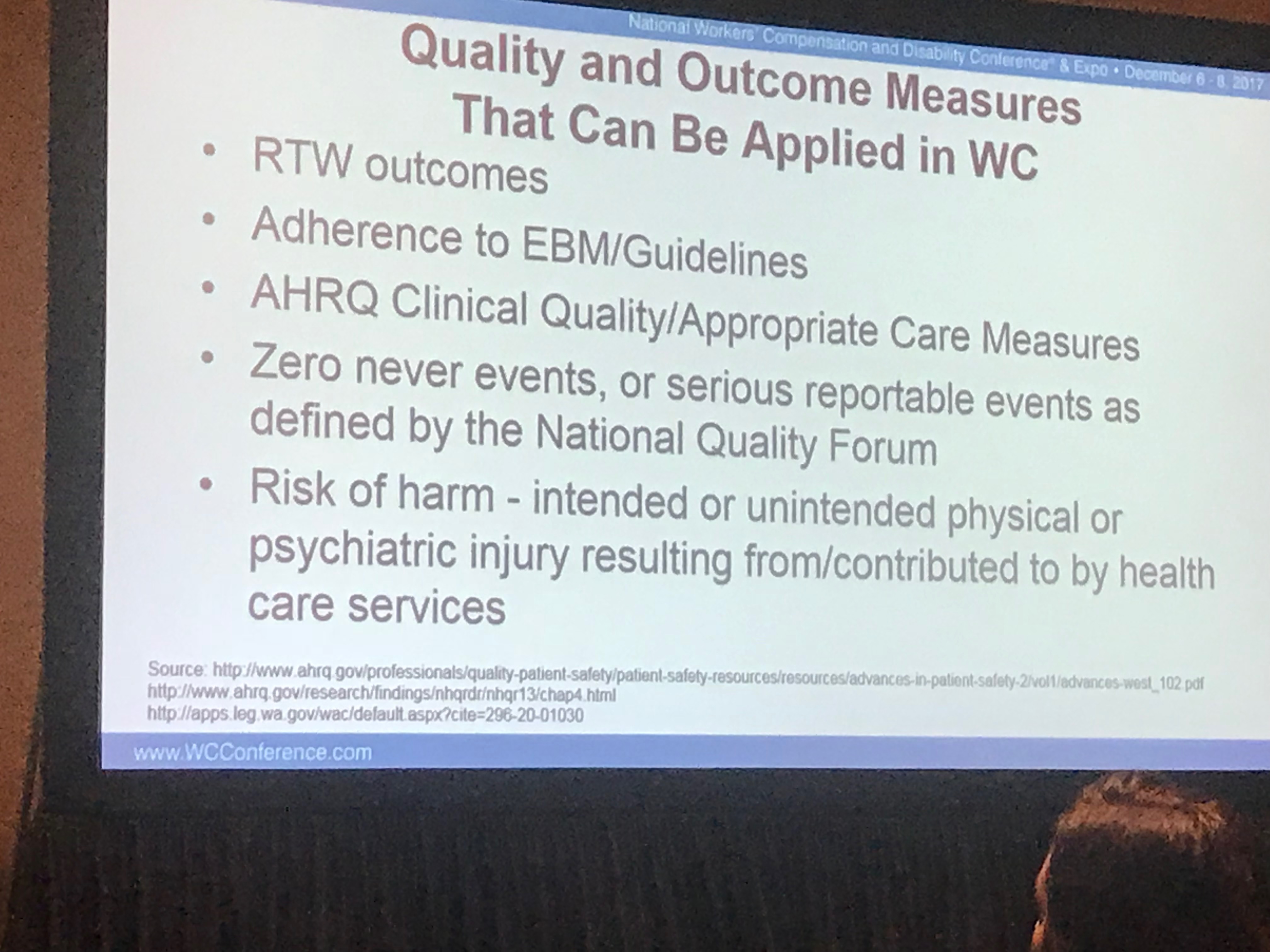

Albertson’s is one of the few large employers challenging this paradigm. Denise shared Albertsons’ network contracting strategy, and of particular interest were the outcomes measures they use. Albertson’s is quite willing to pay for better outcomes, and is diligent in tying outcomes to providers.

So what can you do?

- Require full disclosure of all fees and side arrangements among and between your TPA and other parties.

- Require reporting of all funds transfers

- Realize you are going to have to pay higher per claim fees and/or higher unallocated loss adjustment expenses.

- Require documentation and reporting on quality measures for all medical care including networks.

- Be willing to pay more for better outcomes.

Joé, Sorry we didn’t connect at the show! Sounds like the financial guarantee program we offer may be part of the answer.

Joe, right before I read your comment about being stunned this is still being discussed I thought that I bet I could find a blog posting from you from at least 10 years ago describing the same situation. At least that long ago (before leaving comp for group and Medicare health, though I’ll be back) while pitching transparency, the risk manager of a very large city told me, “I know our TPA vendor is saving us money because they told me so.” That is certainly a mindset we come across often in comp. I believe we are seeing a combination of level of sophistication, misalignment of incentives, and a risk adverse mind set among decision makers.

Absolute agreement Mr. Paduda. Humanizing the system and eliminating backdoor agreements has been a key to our small company’s survival and the success of our claims management against the larger firms.

More thoughts on this here – https://www.facebook.com/MidlandClaimsService/

Thank you for addressing this situation.

mm

Joe I have been attending these meetings for many years and have heard the same message by leaders and thought provokers in the industry (like Denise, Frank and many others), but, as you point out, not much changes. The majority of employers just do not seem to be engaged or truly understand the financial arrangements going on behind the scenes. They subscribe to the smoke and mirror show many of the industries vendors promote as savings. Real savings is providing timely, aggressive correct care and returning people to work efficiently and fully productive. It is pretty simple actually.

Joe,

We couldn’t agree more. The “workers’ compensation industrial complex,” as some have been using the term, has been alive and well for decades. It’s been well publicized in California that loss adjustment expenses are now a larger proportion of costs than either indemnity or the hands-on medical care of injured workers. At our urging more than eleven years ago, the then Insurance Commissioner Steve Poizner helped to bring this to light when he forced California’s Workers Compensation Insurance Rating Bureau to collect and report the costs of cost containment programs separately from actual medical costs. Without that transparency, the industry operates with impunity simply because the fees – and “sharing” arrangements – are charged to the claim file, reported as a medical cost and recovered in premium payments. A relatively recent, but prime, example is your reporting about re-coding of physical therapy bills by third party billers. The practice remains rampant today. Time will tell if the “news” that Mr. Pennachio and Ms. Algire communicated will change the marketplace substantively.

Thanks Steve. Notably a lot of those cost containment expenses in the Golden State are due to a very small population of docs in the LA County area that refuse to practice appropriate medicine. Eliminating those physicians would go a long way to reducing all types of cost.

There’s no question about bad actors on both sides of the fence. Since the article focused on cost containment fees that have run amok, my comments were in reference to them. How did that translate into physician fees?

Steve – actually, the post focused on transparency, employers paying a fair price, AND cost containment costs.

And you didn’t specify “medical cost containment fees”, you said “loss adjustment expenses” – which is a much broader category of which cost containment expenses are but one piece.

Pay for performance is something that will eventually separate the winners from the losers in the next phase of risk management. This will be true in the years ahead for payers, TPAs, vendors, and providers. Now is a good time to think hard about what that means for all of us.

The fact that “uncomfortable truths” continue to persist is because employers haven’t forced regulators to do something about it. Perhaps one or more of the DOZENS of self-insured organizations that are out there might be willing to pursue any of the following regulatory solutions:

1. Expressly prohibit 3rd party vendors from being allowed to make changes to bills that are received from providers. Any changes to bills should ONLY be the responsibility of the provider…Duh! The fact that this hasn’t been addressed over the last few years in the wake of stories that have surfaced is astonishing.

2. Require EDI reporting to be “unbundled” when vendors are responsible for issuing payment to providers. Why track ALAE when a large chunk of it vanishes in situations where vendors function as the proxy ‘payer’ for a medical procedure/service? In practice, ALAE is under-reported as there isn’t a regulatory body anywhere in the WC system who knows how much of medical spend made to vendors is ALAE vs. payments that are actually received by providers. Your regulators should be at least a little curious, no?

3. Require disclosure to employers from TPAs who receive any form of remuneration from their vendor partners. If any dollars that are issued on ‘medical losses” find their way back to the TPA then employers should at least be made aware of it. Interestingly, if an insurance payer is handling their own claims then such a practice is already prohibited as payers aren’t allowed to raid the claims loss ‘piggy bank’, no? How many insurance payers own TPAs who do it? By extension; isn’t some of that $$ getting back to the payer??? (A big mess for sure!) Instead of throwing out the baby with the bathwater we should, at the very least, require disclosure.

4. If a fee schedule exists in your state then vendors calculating “savings” below billed charges where that fee schedule is applied should be expressly prohibited. As reflected in Joe’s article ethics knows no bounds here. The fact that employers are still agreeing to such arrangements is due mostly to clever marketing…it is WAY OVERDUE for regulators to step in to protect uninformed employers.

It would be fantastic to see if anyone would like to comment upon or add to the above…

Mr. Shute, Your comments are well taken and the steps you suggest are a sound place to begin creating the necessary accountability.

I thought that providers must bill according to the WC fee schedule if the claim is known to be WC.

What am I missing?

How do providers then know that they are paid correctly (if they do not know the fee schedule)?

If providers billed correctly, then there is no need for bill review.

EH – thanks for the question.

Providers can bill whatever they want in most states. In addition, bill review does much more than just repricing to the fee schedule; rules such as PT cascading, NCCI edits, clinical edits, and retro UR are all part of bill review – and a lot more.

hope that’s helpful – Joe