This election is about your health and your family’s, because:

Dan Mendelson, CEO, Avalere

(Note to readers – this isn’t a “liberal” or Democratic post, it is a factual description of reality. If you disagree, please provide citations to support assertions)

Today, you are protected because under current law (the ACA, aka “Obamacare”) insurance companies can’t refuse to provide coverage or charge you more if you have a medical condition.

Those protections will go away if Republicans have their way.

According to Avalere,

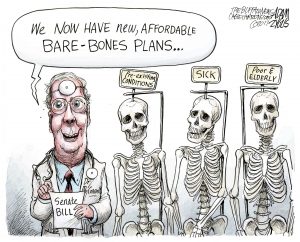

Over 50% of Americans enrolled in coverage outside of the major public programs could face medical underwriting or be denied access to coverage or care without the protections for people with pre-existing conditions contained in the ACA.

Here’s why.

- Last year Republicans came within one vote of repealing the ACA – with NO replacement plan in place.

- Senate leader Mitch McConnell has said he will try to repeal ACA next year.

- House Republicans voted over 54 times to repeal ACA – with NO replacement plan in place.

- The “short-term” and “association” healthplans proposed by Republicans let insurance companies charge you anything they want if you or a family member have a pre-existing condition.

- These short-term and association healthplans can pick and choose what healthcare services they cover – they don’t have to cover drugs, pregnancy, or emergency room care, or anything else they bury in the fine print.

- Republicans are backing a lawsuit that would overturn the ACA in its entirety – and many of the Republicans behind the suit are running for Congress.

If you or someone in your family has had:

- heart disease, high cholesterol, or high blood pressure

- anxiety or depression or any other mental health condition

- obesity

- diabetes

- cancer

- or is pregnant,

your healthcare is at risk.

I have no problem whatsoever with principled Republicans – or anyone else – wanting to overturn the ACA. I have a big problem with anyone who’s lying about what they are doing.

Fact is the GOP has tried over 50 times to let insurance companies refuse to cover your pre-existing conditions, they are pushing a suit that would do the same thing, their bills in Congress will let insurance companies charge you anything they want, yet they are claiming they will protect you.

That’s just a lie.

What does this mean for you?

Do you want insurance to cover your pre-existing medical conditions?

What does this mean for you? You ask… it means I’ve voted early & I was out at my local train station at 6AM this morning. My son has diabetes, my daughter-in-law is pregnant, and I have other pre-existing conditions. We all need PROTECTION!

Thanks Ciasta – democracy requires all of us participate – thanks for doing this.

Joe

My husband is 63. He receives $5,000 per year from his previous employer for ACA. He is not eligible for any premium decrease because we make a few thousand dollars more than the cut point of $62,00/year. He just received his new 2019 premium info from BC/BS of South Carolina: $1,011.92 per month. The $416 per month he receives from his employer brings his total premium out of pocket expense down to $595.92 per month ($7,151.04 per year). His deductible is $7,500per year. He had knee surgery this year and we figured out that we have spent a total out of pocket of $13,643! This is a lot of money for two people, one of which is on Medicare,) with our existing income. We have friends who are self employed and report very little income. They each pay about $30 per month for their healthcare through ACA. Don’t see how this is equitable. I’m almost 69 and still working due to the ACA premiums and deductible There were certainly “lies” told on both sides regarding ACA. My husband and I have no other insurance options for him, as no other insurance provider offers ACA in the state of SC, and he is not old enough to get Medicare.

Hello Martie –

Thanks for the note. There are a couple of points that are relevant here.

1. Under ACA insurers are prevented from charging older folks like us more than 3 times what the youngest people pay. Before ACA, insurers could charge 5 times more. http://us.milliman.com/uploadedFiles/insight/2017/MillimanACAAgeBands_0131_Final.pdf

So, while his premiums are going up, he’s protected from a much higher rate.

2. Healthcare costs are the driver of health insurance costs – they make up 85% or so of premiums. BC/BS just isn’t doing its job controlling cost.

3. Your friends are cheating you and other taxpayers. That is fraud. Of course, I agree that isn’t equitable, it’s illegal.

4. Republicans killed off subsidies designed to help new insurers get started; I’ve written on this extensively. They also eliminated Cost Sharing Reimbursement funds, which went a long way to reducing premiums. Now, the GOP’s removal of the penalty for no insurance has forced insurers to raise rates to account for a sicker population which will happen when young folks drop out of insurance.

I appreciate your frustration. I’m 60, my bride is 59, and we pay a fortune.

That said, I would suggest the vast majority of lies about ACA has come from the GOP. If you have other sources, please let me know.

I have worked for 6 different employers during my 40 year career and never had an issue with employer sponsored health care excluding pre-existing conditions (pre or post ACA) Individual plans, have historically had pre-existing exclusions and I agree that this is an issue that needs to be addressed. I don’t believe that all employer sponsored health care will begin eliminating coverage for pre-existing conditions if this is passed.

Hello Mike – thanks for the note.

Historically small employers usually had to deal with medical underwriting, which affects rates for older and sicker employees. I worked for an insurer and sold this type of policy decades ago. The ACA prohibits this for smaller employers; while this is not specifically excluding pre-ex coverage, it does the same thing – coverage is prohibitively expensive.

Joe