Sean Cooper and Raji Chadarevian delivered perhaps the most useful presentation I’ve seen at any NCCI Conference…There’s a LOT 0f important – and very timely – information in their presentation, so I strongly encourage you to watch it – or watch it again here.

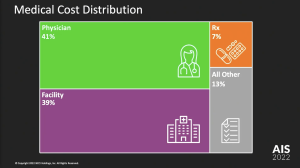

Let’s start with the top line – facilities and physicians (which includes physical medicine as well as MD costs) are by far the biggest chunk of spend. Note that NCCI reports annual drug spend is down to 7% of total spend. This aligns closely with what I’ve been reporting for some time.

The key takeaways…

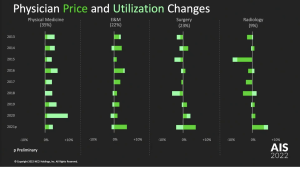

The discussion focused on medical prices – which are the single biggest driver of total US healthcare inflation (see here for more details on this) – and utilization. Disaggregating cost increases provides/ed the audience with a deeper understanding of drivers – well done.

We are approaching network saturation.

Fully 75% of Physician services were delivered in-network – and, as in-network prices grew much more slowly than non-network, this helped reduce overall medical inflation.

Physical medicine is increasing…which is good.

The cost of physical medicine has been increasing while costs for surgery costs have not. What’s driving PM costs is mostly more utilization – indicated by the light green shading below. That is NOT necessarily – or even likely – a bad thing…A course of PT is way less expensive than the costs associated with a surgical episode.

Facilities

Sean noted facility costs have been “the biggest driver of increased medical costs in workers comp” – increasing twice as fast as physician services. (Long-time readers will recall I’ve been banging on this drum ad nauseam.)

There are a host of reasons for this – led by consolidation in the healthcare services industry (also covered in detail here at MCM). Net is when a hospital or health system buys physician practices, it gets to add a facility charge to the what used to be just a physician office bill.

Voila! Instant profit simply by changing the “place of service”. That’s why private equity firms, large health care systems, UnitedHealthGroup, and dominant hospitals have been snapping up physician groups – they are gaming the system.

There’s more to unpack here – which I’ll do early next week.

What does this mean for you?

It’s facility costs.

Joe, Thanks for the insights and report. Not having listened to the program (yet) and with apologies if NCCI covered my question. Facility cost increases, as you mention are a driver that must be mitigated because “place of service” cost increases are not an indication of more or better care, just more expense. Did NCCI attempt to breakdown how much of the increase in physical medicine costs actually land on the rendering provider’s bottom line vis e vis the networks’ that control patient flow and reimbursement? Just as with your example of the practice gobbled up by a hospital, what is “spent” on care, often has no correlation to what is reimbursed to the actual provider of that care. As you’ve pointed out many times, middlemen of all stripes seem to find ways to take what’s spent and keep a disproportionate share, thus needlessly increasing cost without providing any value.

Hello Steve and thanks for the note.

I don’t think anyone has data to identify how much of a payment for medical services ends up as profit for the provider that delivered the service. With so many providers on salary, my guess is this is unknowable.

be well Joe